DATs not going to last

A review on the treasury landscape, and its future

Introduction

The last ‘traditional’ bubble cryptocurrencies experienced was in Q4 2017, characterised by double or even triple digit % days, an influx of new participants such that exchanges couldn’t keep up with demand, speculative ICOs, record volumes, new paradigms, new heights and first class flights. That was the last, mainstream, traditional retail bubble culminating 9 years after the first “trustless” peer-to-peer currency was created.

Fast forward 4 years, and crypto’s second major bubble was larger, more complex, layered in a new paradigm of algorithmic stablecoins (Luna Terra), with a sprinkling of re-hypothecation crime (FTX, Alameda). Such was the ‘innovation’ that few really understood how the largest retail Ponzi-esque collapse worked. But as in every new paradigm, participants were convinced this was a new form of financial engineering, a new form of innovation, and if you didn’t get it, no one had time to explain it to you.

DATs Arrive (2020–2025)

Little did we know at the time, that Michael Saylor’s Microstrategy born in 2020 would be the seed that sprouted institutional-grade re-positioning into BTC after its dramatic collapse in 2022 [1]. So much so, in 2025, Saylor’s “financial alchemy” is now at the heart of marginal buyer demand in cryptocurrencies today. Much akin to 2021, very few truly understand the mechanism behind this new paradigm of financial engineering. Although few understand, a growing number are more wary after previous experiences of what feels and smells dangerous; but how this happens, along with its secondary effects is what makes the difference between knowing something may be wrong, and capitalising on it.

What is a DAT at the base level?

Digital Asset Treasuries (DATs) are pretty simple vehicles. They are traditional equity companies whose sole purpose is to purchase digital assets. New DATs simply raise money from investors, selling shares in their company, and using the proceeds to purchase Digital Assets. In some cases, they continue to sell equity, diluting existing shareholders to use the proceeds to continue purchasing Digital Assets.

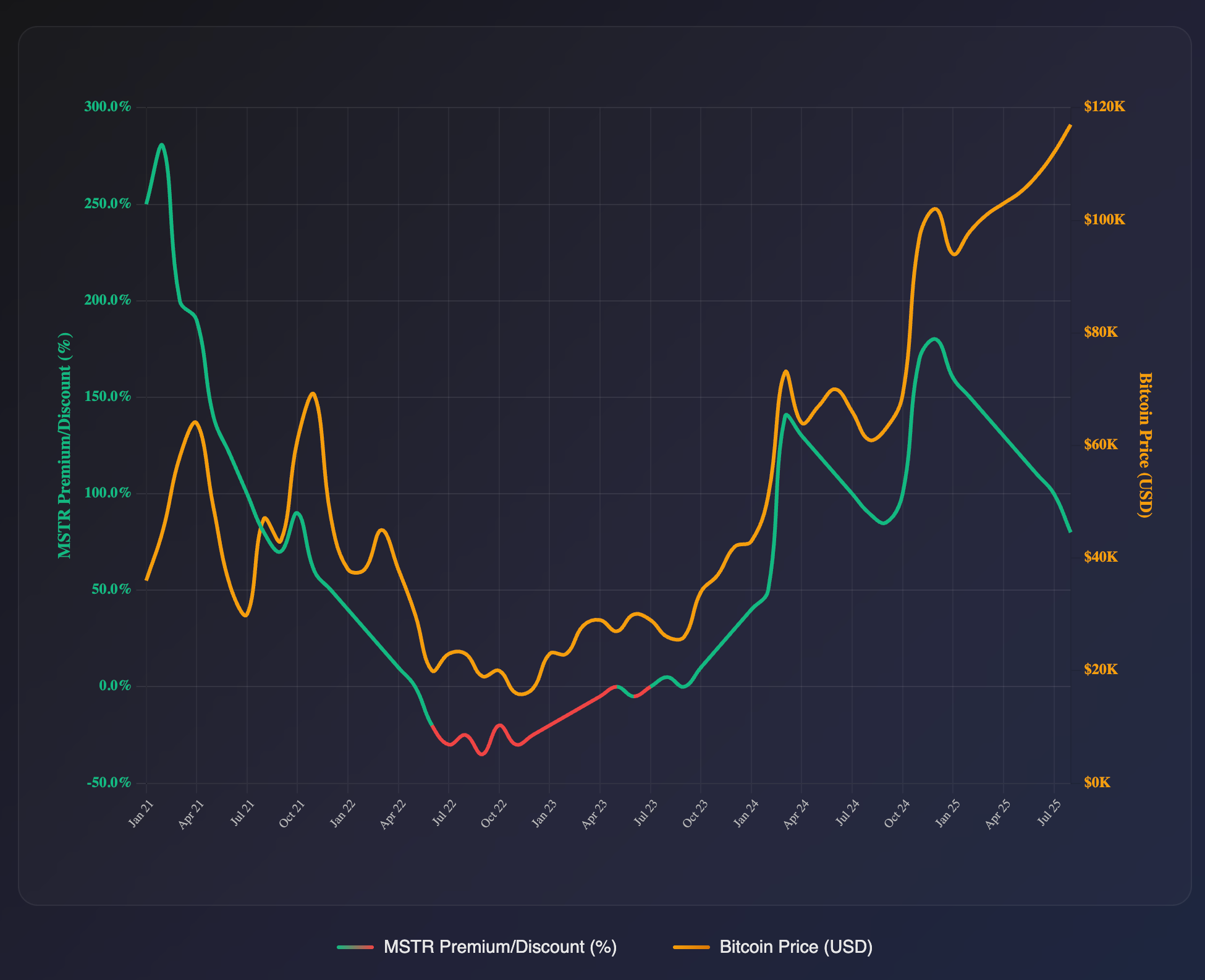

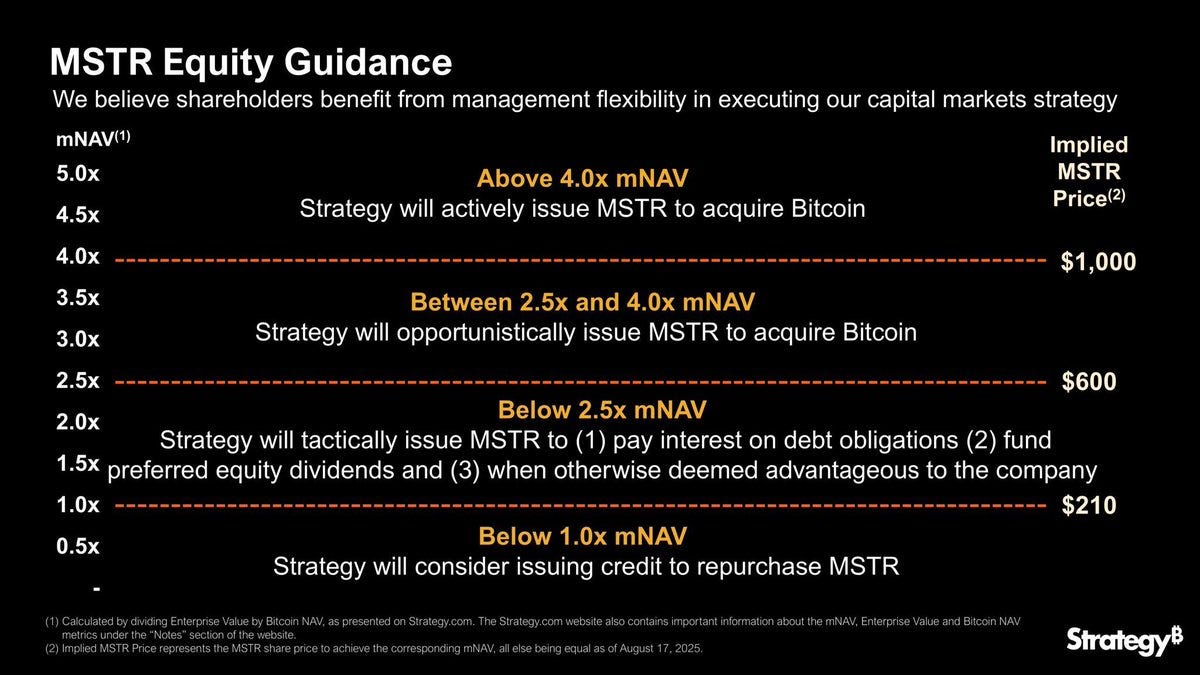

A DAT’s NAV is simple: assets minus liabilities, divided by shares. But the market doesn’t trade NAV, it trades mNAV, the market’s valuation of those shares relative to their underlying assets. If investors pay $2 for $1 of BTC exposure, that’s a 100% premium. This is the alchemy: at a premium the company can issue shares and buy BTC accretively. At a discount, the logic reverses — buybacks or activist pressure dominate.

In this kernel lies the ‘alchemy’. Given that these are new products, that are

A) Exciting (SBET surged 2,000% in one day of trading)

B) Have high volatility

C) Seen as a new paradigm of financial engineering

The reflexive flywheel

SO, with this alchemy, Michael Saylor’s Microstrategy has been trading at a premium to its NAV over the last two years, enabling Saylor to issue shares, and purchase more BTC without significantly diluting shareholders and the share price premium. In this case, it’s also a very reflexive mechanism:

mNAV premium allows Saylor to —> issue equity —> purchase BTC —> BTC increases in price → raising his NAV & share price —→ attracting more investment with a solid premium ——> further raises and purchases. [2]

For the first time in its history it looks as though the discount which has been strongly correlated with Bitcoin’s price has diverged from price; perhaps as a function of other DATs launching in the market. However, this could mark a key turning point as Microstrategy’s ability to continue raising capital to improve this flywheel has diminished as their premium has sunk. It’s worth keeping a strong eye on this; in my view I don’t see this premium returning meaningfully again.

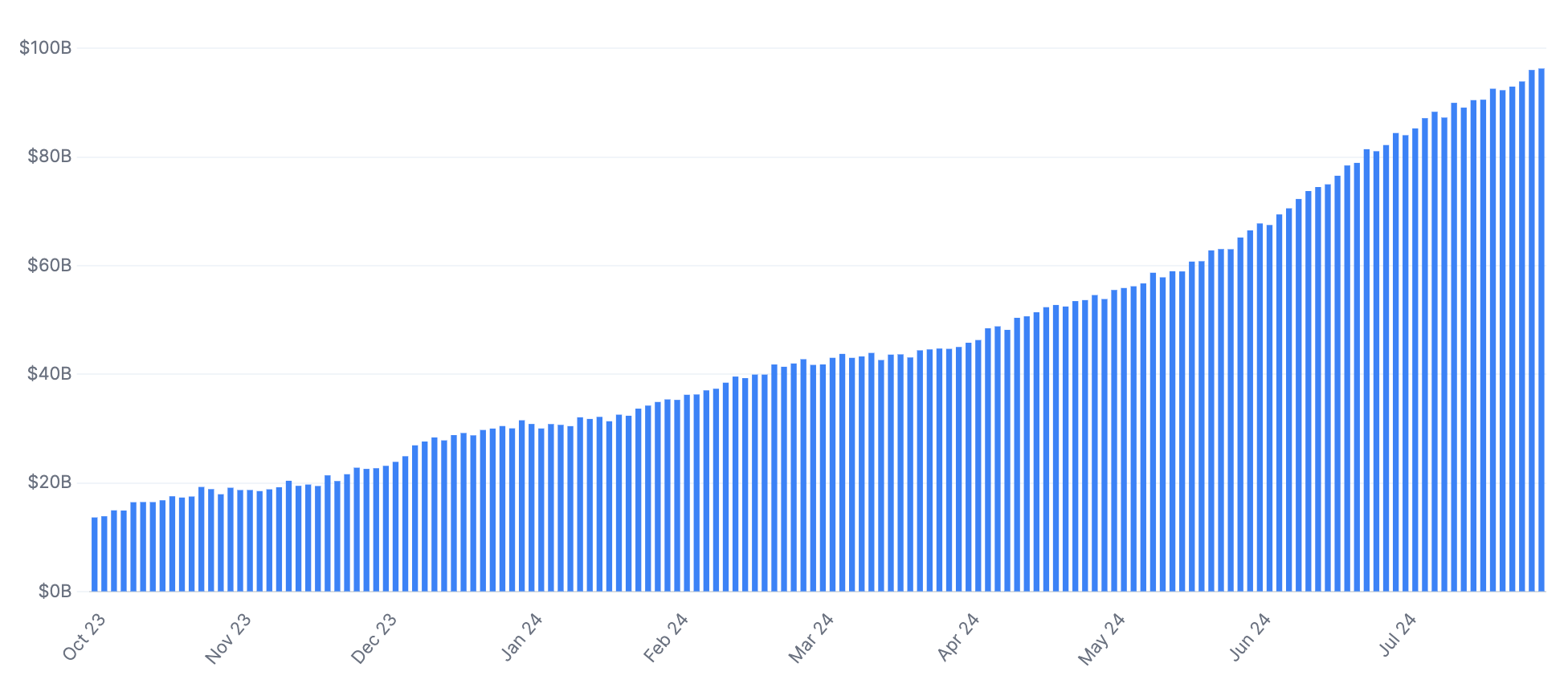

There is no doubt with DAT NAV rising from $10bn in 2020 to over $100bn today, this vehicle has provided significant liquidity to the market, comparable to the sum of all BTC ETFs at $150bn. It has also driven a very reflexive price mechanism into the underlying asset in what have been positive risk conditions for all risk-on assets including BTC [3]

Why it breaks

I don’t see a multitude of different paths for this to play out, it seems clear to me there are only three paths, and one logical conclusion:

DATs continue to trade at premiums to mNAV, the flywheel continues, insatiable demand drives crypto higher. It is simply a new paradigm driven by financial alchemy.

DATs begin to trade at discounts, unwinding until there are forced liquidations and chapter 11’s, total destruction.

DATs begin to trade at discounts, and begin to be forced to sell underlying assets to re-purchase shares/service debt & operating costs. This unwind becomes recursive, until these DATs reduce in size creating DAT ghost companies.

I find it highly unlikely DATs continue to trade at premiums; my opinion is this premium is a function of loose liquidity conditions for risk assets, which have benefitted NDX stocks, and equity prices in general. When liquidity conditions were tighter during 2022/3 it’s clear there were no premiums on MSTR, and in short periods there were discounts. This, is the first area I think there is mis-pricing, premiums should not exist for DAT companies period; in fact these companies should be trading at a DEEP discount to NAV.

The reason for that is the implied equity value of these companies is a function of their ability to return shareholder value; traditional companies do this through dividends, share buybacks, acquisitions, growth expansion and so on. DATs do not have this capability, their only capability is either to issue equity, issue debt, or do some minor treasury actions such as staking, which is broadly insignificant. So what’s the value in holding their equity? Well, hypothetically, the value of these DATs is their ability to return their NAV back to their shareholders, otherwise there isn’t much value in the equity. But given none of these vehicles have enabled this possibility, and several have committed to never selling any of their underlying assets, the equity value in this case is worth as much as someone is willing to pay for it.

Ultimately the equity value is now a function of:

The probability of future buyers creating a premium (based on the DATs ability to continue raising capital at a premium)

The price of the underlying asset & liquidity of the market to absorb sales

The implied probability that the shares can be reedemed for NAV

If DATs were able to return capital to shareholders, this would be akin to an ETF, but given they’re not, I argue this is much closer to a closed-end fund than it is to anything else. Why? Because it’s a vehicle that owns an underlying asset with no mechanism to distribute the value of those assets to its investors. For those with good memory, this reminds me distinctly of GBTC & ETHE, both of which were also part of the significant unwind in 2022 when the closed-end funds’ premium quickly sank to a discount [4]. This unwind essentially was priced as a function of liquidity and implied probability of future conversion. Given that there was no way to redeem GBTC, the same as DATs, the market in liquid conditions when demand was high priced in a premium, but when underlying prices fell and began contracting, this discount became very apparent as the trusts reached 50% discount to NAV. Ultimately this haircut to NAV was the price investors were willing to pay for an asset which had no logical or foreseeable option to distribute its NAV value to holders of the trust; so pricing was based on its potential to do so in the future and demand for that liquidity.

Debt and Secondary Risks

In the same way, DATs only ability to generate value for shareholders is two-fold outside of returning capital is through treasury management (staking) & raising debt. If we see DATs begin to raise significant debt, that would be a signal to me that an aggressive unwind is due to take place, although I think debt raising is unlikely. Either way, in both scenarios, these two options of generating value pale in comparison to the share value of the assets held by the company, and consequently is ever-reminiscent of GBTC. If this analysis is the case, it’s only a matter of time until investors begin to realise this too and the bubble of confidence is popped; leading to the recursive loop of declining premiums into discounts and potentially selling of underlying assets.

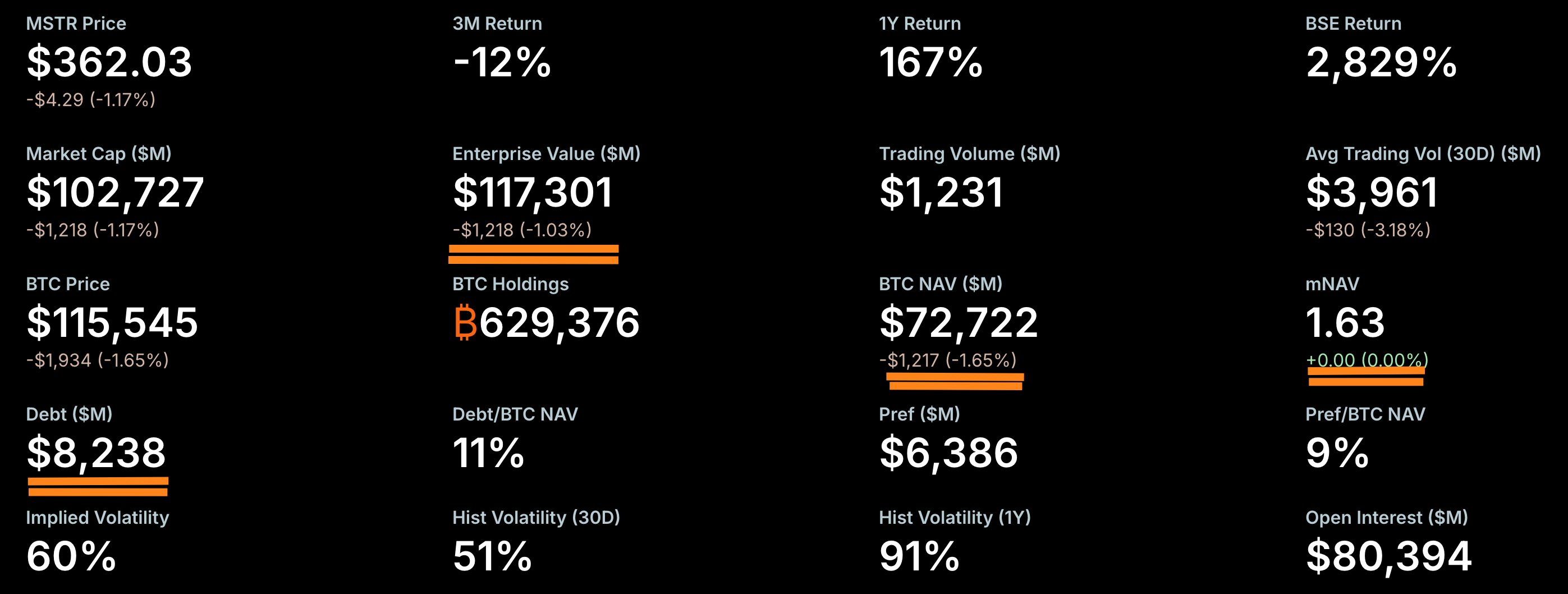

Now, I find it highly unlikely also there will be any forced liquidations or chapter 11’s in regards to any leverage or debt winding down. This is because there is simply not enough debt to be problematic for Microstrategy, or any other DAT given the preferred fundraise of choice is equity offerings. With debt at $8.2bn & holdings at 630,000 BTC, BTC price would have to be $13,000 before debt>assets, which I find highly unlikely [5]. BMNR & other ETH DATs also have little to no leverage, so forced liquidation is unlikely to be the poison of choice. Much more likely for DATs outside of MSTR is that they wind down returning capital to shareholders either through activist acquisitions or shareholder voting. All of that acquired BTC & ETH then, is likely to head straight back into the market from whence it came.

Saylor’s Choice

Saylor owns the majority (50%+) of voting rights in Microstrategy although he only owns roughly 20% of the equity. Therefore it’s almost impossible for an activist fund to force any share selling or any collective of investors. One consequence of this may be if MSTR begins trading at a significant discount, and there’s no way for investors to force share buybacks, there may either be investor lawsuits or regulatory oversight which could cast even more of a shadow onto the share price.

Generally what worries me is that there is a saturation point where additional DATs are no longer affecting price, improving the reflexivity of these mechanisms. At which point, after there’s enough supply to absorb artificial & immature DAT demand, the unwind will begin to take place. To me, it looks as though that is a not too distant future.

Having said this, Saylor’s ‘debt’ theory is massively overblown. He simply doesn’t own enough today to be problematic imminently. His convertibles, in my view will have to be redeemed in cash at par, because I think his equity will tumble significantly if there are mNAV discounts.

One thing to keep an eye on is whether he issues more debt if mNAV<1 to do share repurchases; I find these highly unlikely to solve the mNAV problem as once investor confidence has tarnished, it’s very hard to drag it back. So continuing to issue debt to solve any problems with mNAV, I think will be a problematic path. Also, MSTR’s ability to raise debt to cover his liabilities will become increasingly difficult if mNAV falls, which will affect his credit rating and investor demand for his products. In this way, issuing more debt could become a reflexive downward spiral.

mNAV falls → investor confidence falls → Saylor issues debt to repurchase shares → investor confidence is still low → mNAV continues to fall → Pressure mounts → More debt issuance (Debt would have to reach meaningful leverage to be dangerous in the near term).

Regulation and Precedent

A much more likely scenario before then is one of two options: 1) Microstrategy faces investor class action lawsuits pushing to return shareholder capital back to NAV 2) Regulatory scrutiny. Position 1 is pretty self-explanatory and may occur if there is a significant discount (below 0.7mNAV). Position 2 is more nuanced, and there’s precedent for this

History shows what happens when companies masquerade as operating businesses but function as investment wrappers. In the 1940s Tonopah Mining was ruled an investment company because it held mostly securities [6] . In 2021, GBTC and ETHE traded at wild premiums only to collapse to 50% discounts. Regulators looked away while investors were winning, but once retail was trapped at a loss the narrative flipped, and conversion to ETFs was forced.

MicroStrategy is in the same position. It still calls itself a software company, but 99% of its value is Bitcoin. It’s equity performing the role of an unregistered closed-end fund with no redemption. That distinction survives only while markets are buoyant.

If DATs trade at persistent discounts, regulators can reclassify them as investment companies, cap leverage, impose fiduciary duties, or force redemptions. They can shut off the equity-issuance flywheel entirely. What was financial alchemy at a premium will be treated as predatory at a discount. This could be Saylor’s true point of vulnerability.

What are the headlines?

I’ve given you subtle hints as to what I think may happen, but now I will make some outright predictions

More DATs continue to launch for increasingly risky and speculative assets signalling impending height of the liquidity cycle

Pepe, Bonk, Fartcoin & others

Competition of DATs dilutes & saturates the market causing mNAV premiums to fall significantly

DATs will converge toward the valuation dynamics of closed-end funds

This can be expressed as a trade through short equity/long underlying to capture mNAV premiums

This trade will have funding costs and execution risks. OTM options is also a way to express this in a simpler way.

The majority of DATs will trade at a discount to mNAV within the next 12 months causing a turning point in bearish crypto prices.

Equity issuance stops. Without new inflows, these companies become “zombies” with static balance sheets. No growth flywheel → no new buyers → lingering discounts.

MicroStrategy endures a collective investor lawsuit OR Regulatory oversight which may cast doubt on its commitment to never sell BTC.

This marks the beginning of the end

The positive view on financial engineering & ‘alchemy’ will quickly turn sour as prices work reflexively on the underlying assets on the way down

Sentiment on Saylor, Tom Lee & others will change from Savants to Pariahs

Some DATs may use debt instruments during the unwind to either purchase shares or purchase more assets → This is a signal of impending doom

The trade here would be to lean into the debt and increase short premium positioning into this

An activist fund will acquire the shares of a DAT at a discount and pressure/force the DAT to wind down and distribute its assets.

At least one activist fund (Elliott, Fir Tree style) will take a DAT position at a steep discount, agitate for liquidation, and force distribution of BTC/ETH back to shareholders. This will set precedent.

Regulatory intervention

SEC could force disclosure rules or investor protections.Historically, closed-end funds with persistent discounts prompted regulatory reform.

Sources

[1] MicroStrategy Press Release

[2] MicroStrategy SEC 10-K (2023)

[3] Bloomberg – “Crypto Treasury Companies Now Control $100bn in Digital Assets”

[4] Financial Times – “Grayscale Bitcoin Trust Slides to 50% Discount” (Dec 2022).

[5] MicroStrategy Q2 2025 10-Q filing.

[6] SEC v. Tonopah Mining Co. (1940s ruling on investment company status).

we are so back

Joe is so back!